Inflation unexpectedly slipped 0.1% (not seasonally adjusted) in June, following a 0.6% increase in May. This was the first decline in six months. The monthly decrease was driven by lower prices for travel tours (-11.1%) and gasoline (-3.1%).

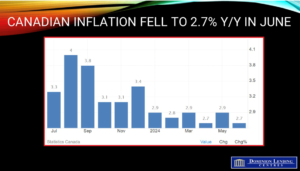

The Consumer Price Index (CPI) rose 2.7% year over year in June, down from a 2.9% gain in May. The deceleration was mainly due to slower year-over-year growth in gasoline prices, which rose 0.4% in June following a 5.6% increase in May. Excluding gasoline, the CPI rose 2.8% in June.

Lower prices for durable goods (-1.8%) y/y also contributed to the slowdown in the all-items CPI in June, following a 0.8% decline in May. An increase in prices for food purchased from stores (+2.1%) moderated the deceleration, as well as a smaller decline for cellular services in June (-12.8%) compared with May (-19.4%).

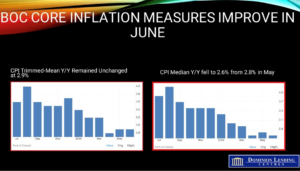

The Bank of Canada’s preferred measures of core inflation, the trim and median core rates, exclude the more volatile price movements to assess the level of underlying inflation. The CPI trim was unchanged in June at 2.9%, above the market’s expectation of 2.8%. The CPI median fell two ticks to 2.6%.

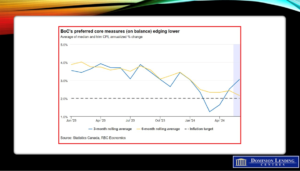

The third chart below shows the 3- and 6-month moving averages for the average of median and trim CPI measured as an annualized percentage change. While the 3-month moving average has accelerated to about 3%, the 6–month measure has fallen to just over 2%.

Bottom Line

Today’s inflation reading is good news for the Bank of Canada, giving them leeway to cut interest rates next week. June marks the sixth consecutive month that the headline yearly inflation rate has been within the BoC’s target range, bringing the annual pace of price pressures back to its weakest levels since 2021.

Today’s inflation data will give the central bank confidence that the May rise in inflation was temporary. Annual inflation will reach the Bank’s 2% target by some time next year. This opens the way for the Bank to cut the overnight rate on July 24 by 25 bps to 4.5%.

According to Bloomberg News, traders in overnight swaps increased their bets that the Bank of Canada would cut rates next Wednesday, putting the odds at about 90% compared with 80% before the release.

Yesterday’s business and consumer outlook surveys point towards slowing growth in firms’ input and selling prices amid a weaker economic backdrop. Inflation expectations fell in June and are now in the BoC’s target range. Businesses are expecting weaker soft demand. The unemployment rate is trending higher, and the share of firms reporting labour shortages is near a record low. Companies’ expectations for wage increases over the next year have slowed. Overall, capacity constraints “have returned close to their historical average.”

The central bank flagged that consumer survey respondents still think domestic factors, including fiscal policy and elevated housing costs, are “contributing to high inflation.” Home-buying intentions are near historical averages, the bank said, and are supported by “strong plans” among newcomers to buy homes.

Another rate cut is coming next week, which will help to spur housing activity

Dr. Sherry Cooper

Chief Economist, Dominion Lending Centres

Image Credit: Stockbyte on Canva