Slower GDP growth and easing inflation trends are likely to influence the Bank of Canada’s upcoming rate decision, offering key insights as we approach their October 23 meeting.

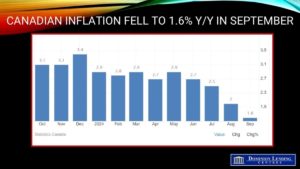

The Consumer Price Index (CPI) rose 1.6% year over year in September, the slowest pace since February 2021 and down from a 2.0% gain in August 2024. The main contributor to headline deceleration was lower year-over-year gasoline prices in September (-10.7%) compared with August (-5.1%). The all-items CPI, excluding gasoline, rose 2.2% in September, matching the increase in August for this measure.

Although the rate at which prices increase has slowed, price levels remain elevated. Compared with September 2021, the CPI rose 12.7% in September. Canadians continue to feel the impact of higher price levels for day-to-day basics such as rent (+21.0%) and food purchased from stores (+20.7%), which increased during that same 3-year period.

The CPI fell 0.4% in September after a 0.2% decline in August. Lower gasoline prices led to both the monthly and yearly movement in September. On a seasonally adjusted monthly basis, the CPI remained unchanged at 0.0%.

The central bank’s two core inflation measures remain sticky. Both measures were unchanged in September (see chart below). According to Bloomberg calculations, a three-month moving average of those measures fell to an annualized pace of 2.1% from 2.3% in August.

According to Bloomberg News, “After the release, traders in overnight swaps upped their bets that the Bank of Canada will opt for a larger rate cut at next week’s decision, putting the odds of a half-percentage-point reduction at about 75%. Previously, the odds were around 50%.” The Canadian dollar weakened further on the news relative to the greenback. The loonie has fallen for ten days, the longest streak since 2017. Canadian debt rallied across the yield curve, outperforming US Treasuries and pushing the two-year Canada benchmark yield to 3.03% and the 5-year bond yield to 2.92% by mid-day.

Tuesday’s data marks the first time since February 2021 that inflation is below the central bank’s 2% target and is the ninth straight month of headline rates running within its target range. With inflationary pressures continuing to ebb and policymakers focusing more on preserving economic growth, the data give the central bank options to reduce rates quicker after cutting borrowing costs at 25 basis points at the past three meetings.

Bottom Line

While the September employment data were stronger than expected, Q3 GDP growth is slated to be roughly 1.8%, well below the Bank of Canada’s 2.8% forecast. Today’s inflation report is the last important data point before the Bank meets again on October 23. Late last month, BoC Governor Tiff Macklem warned that growth may be below policymakers’ previous expectations in Q3.

Excluding shelter costs, the consumer price index rose 0.4% from a year ago compared to 0.5% in August. Mortgage interest costs and rent remained the most significant contributors to the annual inflation rate change. However, rent prices increased at a slower pace in September, rising 8.2% versus 8.9% in August. Tuition fees, priced annually in September, also grew slower, increasing 1.8% compared with 2.5% last year.

Regionally, inflation is now at or below 2% in every province, with prices rising slower in September than in August in all ten provinces. The central bank will release new economic forecasts in the Monetary Policy Report next week. Macklem has said, “decisive monetary policy action and the unblocking of supply chains” means “uncertainty about costs and inflation are much lower today than two years ago”.

Dr. Sherry Cooper,

Chief Economist, Dominion Lending Centres

Image Credit: Andre Hunter Unsplash